When the Paycheck Stops: How I Navigated Unemployment with Smarter Money Moves

You wake up, coffee in hand, and check your email—only to find a termination notice. That sinking feeling hits hard. I’ve been there. When my job disappeared overnight, panic set in fast. But instead of freezing, I turned to a plan built on real strategies: cutting costs without chaos, stretching savings wisely, and protecting what mattered most. This is not a theoretical guide—it’s what actually worked when everything felt uncertain. In the days that followed, I learned that financial resilience isn’t about having the biggest salary or the most luxurious lifestyle. It’s about making thoughtful, disciplined choices when the ground shifts beneath you. This is how I navigated the storm—and how you can too, if you ever face the same.

The Moment Everything Changed

The email arrived at 8:17 a.m. on a Tuesday. No warning, no conversation—just a brief message stating my position was eliminated due to restructuring. I read it twice, then a third time, hoping I had misunderstood. My hands trembled as I closed the laptop. The silence in the room felt heavier than usual. For a moment, I couldn’t move. The reality wasn’t just the loss of income—it was the collapse of routine, identity, and security. I had worked at that company for nearly eight years. My job wasn’t just a paycheck; it was part of who I was. In that instant, everything changed.

Emotionally, the days that followed were a blur. There was disbelief, anger, and waves of anxiety that came without warning. I found myself checking my bank balance multiple times a day, calculating how long my savings would last. I avoided calling friends, ashamed to admit what had happened. The stigma of job loss, even when it’s completely out of one’s control, can be isolating. But beneath the emotional turmoil, a practical question emerged: What do I do now? The answer wasn’t immediate, but I knew that reacting out of fear would only make things worse. I needed to pause, assess, and act with clarity.

That first week, I allowed myself one full day to grieve. I cried, journaled, and talked to my spouse about our fears. But on day two, I made a decision: I would treat this crisis like a project. I created a folder labeled “Financial Recovery Plan” and began gathering documents—bank statements, bills, retirement accounts, insurance policies. I listed every monthly obligation and every source of potential income. This simple act shifted my mindset from victim to strategist. It didn’t erase the pain, but it gave me a sense of control. I realized that while I couldn’t control how I lost my job, I could control how I responded. That shift in perspective became the foundation of everything that followed.

Stabilizing the Financial Foundation

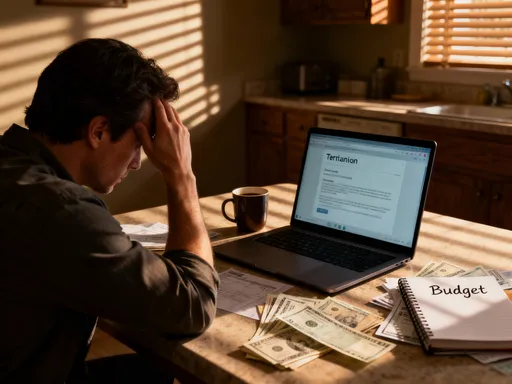

When regular income stops, the first priority is not to panic—but to stabilize. This means securing the essentials: shelter, food, utilities, and healthcare. The instinct during a crisis is often to slash every expense immediately, but that approach can backfire. Drastic cuts often lead to frustration, burnout, or even more spending later when restrictions feel too tight. Instead, I focused on creating a sustainable bare-bones budget—one that preserved dignity while conserving cash.

I started by categorizing my expenses into three tiers: non-negotiables, flexible obligations, and discretionary spending. Non-negotiables included rent, car payment, health insurance, and groceries. These were the costs that, if missed, would trigger late fees, service interruptions, or long-term consequences. Flexible obligations included subscriptions, phone plans, and minor debts. These could be renegotiated or paused. Discretionary spending—dining out, entertainment, travel—was suspended entirely. I didn’t eliminate these permanently; I simply pressed pause, knowing I could revisit them later.

One of the most effective steps I took was negotiating with service providers. I called my internet company and explained my situation. Within ten minutes, I was switched to a lower-tier plan with a six-month discount. I did the same with my phone carrier and managed to reduce my monthly bill by nearly 30 percent. These small changes added up. At the same time, I avoided closing credit cards or canceling accounts impulsively. Doing so could have negatively impacted my credit utilization ratio, which plays a key role in credit scoring. Instead, I used them minimally and paid off balances in full each month to maintain a positive record.

Emotional discipline was just as important as financial discipline. I reminded myself daily that this was temporary. I set small goals—like staying within my grocery budget for two weeks—and celebrated when I met them. I also limited how often I checked my bank account, choosing specific times each week to review my balance. Constant monitoring only fueled anxiety. By creating structure and routine, I was able to maintain stability even without a steady paycheck. The goal wasn’t austerity; it was sustainability. And that made all the difference.

The Emergency Fund: Lifeline or Illusion?

Before I lost my job, I believed I was prepared. I had saved six months’ worth of expenses in a high-yield savings account—what financial experts often recommend. But when the crisis hit, I quickly realized that theory and reality are not the same. My emergency fund wasn’t an endless supply of cash; it was a finite resource with an expiration date. Every withdrawal brought me one step closer to zero. The question became: How do I make it last?

Many people assume an emergency fund is meant to replace income dollar for dollar. That’s a dangerous misconception. In practice, I found that using my savings to maintain my pre-layoff lifestyle would have depleted the fund in less than three months. Instead, I adopted a tiered withdrawal strategy. I divided my emergency savings into monthly allocations, each slightly lower than my previous monthly spending. This created a gradual transition into a lower-cost lifestyle, reducing the shock of sudden frugality.

I also made a strict rule: no withdrawals for non-essentials. That meant no online shopping, no impulse purchases, no “just this once” exceptions. I treated the fund like oxygen in a submarine—valuable, limited, and only to be used when absolutely necessary. I tracked every dollar spent and reviewed my usage weekly. This level of awareness helped me spot patterns. For example, I noticed that grocery costs spiked when I shopped without a list. Switching to meal planning and buying in bulk reduced my food expenses by nearly 25 percent, extending the life of my savings.

Another common mistake I avoided was dipping into retirement accounts. Withdrawing from a 401(k) or IRA before age 59½ typically triggers taxes and a 10 percent penalty. That means losing nearly a third of the amount withdrawn before you even spend it. While the temptation was real, I knew that sacrificing long-term security for short-term relief would only deepen the crisis later. Instead, I protected those accounts and relied solely on my emergency fund and new income sources. In the end, my savings lasted eight months—two months longer than projected—because I used them wisely, not desperately.

Income Alternatives That Actually Work

While cutting expenses buys time, replacing income is the true path to recovery. I knew I couldn’t rely on savings forever. I needed to generate cash flow, even if it wasn’t at my previous salary level. The challenge was finding opportunities that were realistic, accessible, and consistent—not just one-off gigs that paid pennies. I explored several options, and while not everything worked, some strategies delivered meaningful results.

Freelance writing was one of the first paths I pursued. I had experience in corporate communications, so I updated my portfolio and joined platforms like Upwork and Fiverr. The initial response was slow. I spent hours applying to low-paying jobs and received few replies. But after refining my profile and focusing on niche areas like financial content and business editing, I began landing higher-quality projects. Within two months, I was earning a few hundred dollars a week. It wasn’t full-time income, but it covered groceries and helped preserve my emergency fund.

Remote tutoring was another viable option. I have a background in education, so I signed up with online tutoring companies that connected me with students needing help in English and writing. Sessions were scheduled in the evenings, which fit around my job search. The pay was modest but steady—around $25 per hour—and the work was fulfilling. More importantly, it kept my skills sharp and my routine intact. Consistency mattered more than the amount. Knowing I had three sessions a week gave me structure and a sense of purpose.

I also explored part-time administrative work through local staffing agencies. These roles were temporary but often led to longer assignments. One placement at a nonprofit lasted four months and eventually turned into a referral for another position. The key was staying flexible and open-minded. I didn’t wait for the perfect job; I took what was available and made the most of it. Over time, these income streams didn’t replace my salary, but they reduced the pressure on my savings and kept me financially active. The lesson was clear: momentum matters. Even small earnings contribute to stability and confidence.

Managing Debt Without Damage

Debt doesn’t disappear when income stops—and for many, it becomes the most stressful part of unemployment. I had two student loans, a car payment, and a small credit card balance. Before losing my job, these payments were manageable. Suddenly, they felt like boulders on my chest. I knew missing payments would hurt my credit, but I also couldn’t afford to pay everything in full. The solution wasn’t avoidance—it was communication and strategy.

My first step was contacting each lender. I explained my situation honestly and asked about hardship programs. To my surprise, most were willing to help. One student loan servicer offered a three-month forbearance with no interest accrual. My car lender allowed me to skip one payment and add it to the end of the loan. These weren’t permanent fixes, but they bought me breathing room. I documented every conversation and kept records of agreements. This protected me from misunderstandings and ensured I followed the terms correctly.

I also prioritized my debts strategically. I focused on secured obligations—those tied to assets—first. That meant protecting my car payment, because losing the vehicle would make job hunting nearly impossible. Next came debts with the highest interest rates. My credit card had a 19 percent APR, so I stopped using it entirely and paid the minimum on time every month. Unsecured debts, like personal loans, were addressed last, after essentials were covered. This approach minimized financial damage while maintaining credibility with creditors.

One trap I avoided was taking on new debt to cover old debt. Balance transfers and consolidation loans can seem appealing, but they often come with fees or variable rates that increase risk. I also ruled out borrowing from retirement accounts or taking cash advances—options that could have created long-term harm. Instead, I stuck to negotiation, prioritization, and temporary relief. Over time, as income returned, I resumed regular payments and even paid down balances faster than before. The experience taught me that managing debt during hardship isn’t about eliminating it overnight—it’s about protecting your credit and staying in control.

Protecting Future Financial Health

Unemployment doesn’t just drain bank accounts—it can erode long-term financial health if not managed carefully. One of my biggest concerns was maintaining insurance coverage. I was no longer eligible for employer-sponsored health insurance, so I enrolled in COBRA, which allowed me to keep the same plan for up to 18 months. It was expensive—nearly $500 a month—but I viewed it as non-negotiable. A medical emergency without coverage could have wiped out my savings entirely. I also kept my auto and renters insurance active, knowing that a single accident or theft could create a secondary crisis.

Another priority was protecting my retirement savings. While I wasn’t earning a full salary, I still contributed small amounts to my IRA when possible—sometimes as little as $25 a month. This wasn’t about growth; it was about maintaining the habit. Research shows that people who stop contributing during downturns often never restart at the same level. By keeping the habit alive, even minimally, I preserved momentum. I also avoided taking loans from my 401(k), which some consider during hardship. While technically allowed, such loans come with risks—if you don’t repay on time, they become taxable income, triggering penalties.

I also began tracking my net worth monthly. This simple practice helped me see the bigger picture. Even during unemployment, I was making progress—paying down debt, avoiding new liabilities, and preserving assets. Seeing that number stabilize, then slowly rise, was incredibly motivating. I also set micro-goals, like reducing my credit card balance by $200 or saving $100 in a separate account. These small wins built confidence and reinforced positive behaviors. Over time, these habits didn’t just support recovery—they laid the foundation for greater resilience in the future.

Lessons Learned and Systems Built

When I finally landed a new job—eight months after my termination—I didn’t just return to normal. I returned with a new financial system. The experience had changed my relationship with money. I no longer saw it as something to be spent or saved in isolation. I saw it as a tool for security, freedom, and intentionality. The crisis had forced me to confront bad habits, test new strategies, and build practices that lasted far beyond the unemployment period.

One of the most lasting changes was my approach to emergency savings. I realized that six months of expenses wasn’t enough for someone with dependents and fixed costs. I now aim for nine to twelve months, and I keep it in a separate, hard-to-access account to prevent temptation. I also diversified my income streams. I continue freelance work on the side, not because I need it, but because it provides a buffer. I’ve also built a stronger network, knowing that personal connections often lead to opportunities when formal channels fail.

Perhaps the most important lesson was adaptability. Financial plans fail not because they’re poorly designed, but because they’re too rigid. Life is unpredictable. Jobs end, markets shift, and emergencies arise. The goal isn’t to prevent every setback—it’s to build a system that can absorb shocks and keep moving forward. I now review my budget, insurance, and savings every quarter. I adjust as needed, rather than waiting for a crisis to force change.

Looking back, I wouldn’t wish unemployment on anyone. But I also wouldn’t erase the experience. It taught me discipline, resourcefulness, and the power of proactive planning. It reminded me that financial security isn’t about perfection—it’s about preparation, persistence, and the courage to act when everything feels uncertain. If you ever face a similar challenge, know this: you are not alone, and you are not helpless. With the right mindset and strategies, you can navigate the storm—and emerge stronger on the other side.